Two Upgrade Offers To Pass On: One From Chase & One From Citi

One thing American Express does better than anyone is upgrade offers. It doesn’t appear that Chase and Citi have figured it out really. I guess they think their cards are so good that a tempting offer isn’t needed, they think the card speaks for itself. In one case I did take a less than compelling offer, for the World of Hyatt card, because the card was that good. But for these latest offers I don’t see what they are thinking.

RELATED: Why I HOPE Citi Adds the 48 Month Rule to ThankYou Cards

Citi ThankYou Preferred to ThankYou Premier Offer

My wife received an offer on her Citi ThankYou Preferred card to the ThankYou Premier card. The offer – a waived annual fee for upgrading. No points for moving over, no spending offer, just a waived $95 annual fee.

This is a pass for me because the ThankYou Preferred card has the best ThankYou points spending offers. Like the recent one that gets 10X points on almost everything. If I upgraded her to the Premier card most of that would go to the wayside. The Premier does have a better earning structure overall but they are overshadowed by our other cards. So the categories are somewhat worthless for me.

The only time I could see it making sense is if you had a lot of ThankYou points in your account and you wanted to unlock transfer partners. But if it has been over 24 months then sign up for the card with a welcome offer. If you wanted to avoid the hard pull for the sake of Chase 5/24 status then maybe it would make sense to upgrade. Or if you recently downgraded the card to the Preferred to avoid the annual fee and you could now upgrade it and avoid the fee another year. But those options are going to be rare occasions in my opinion.

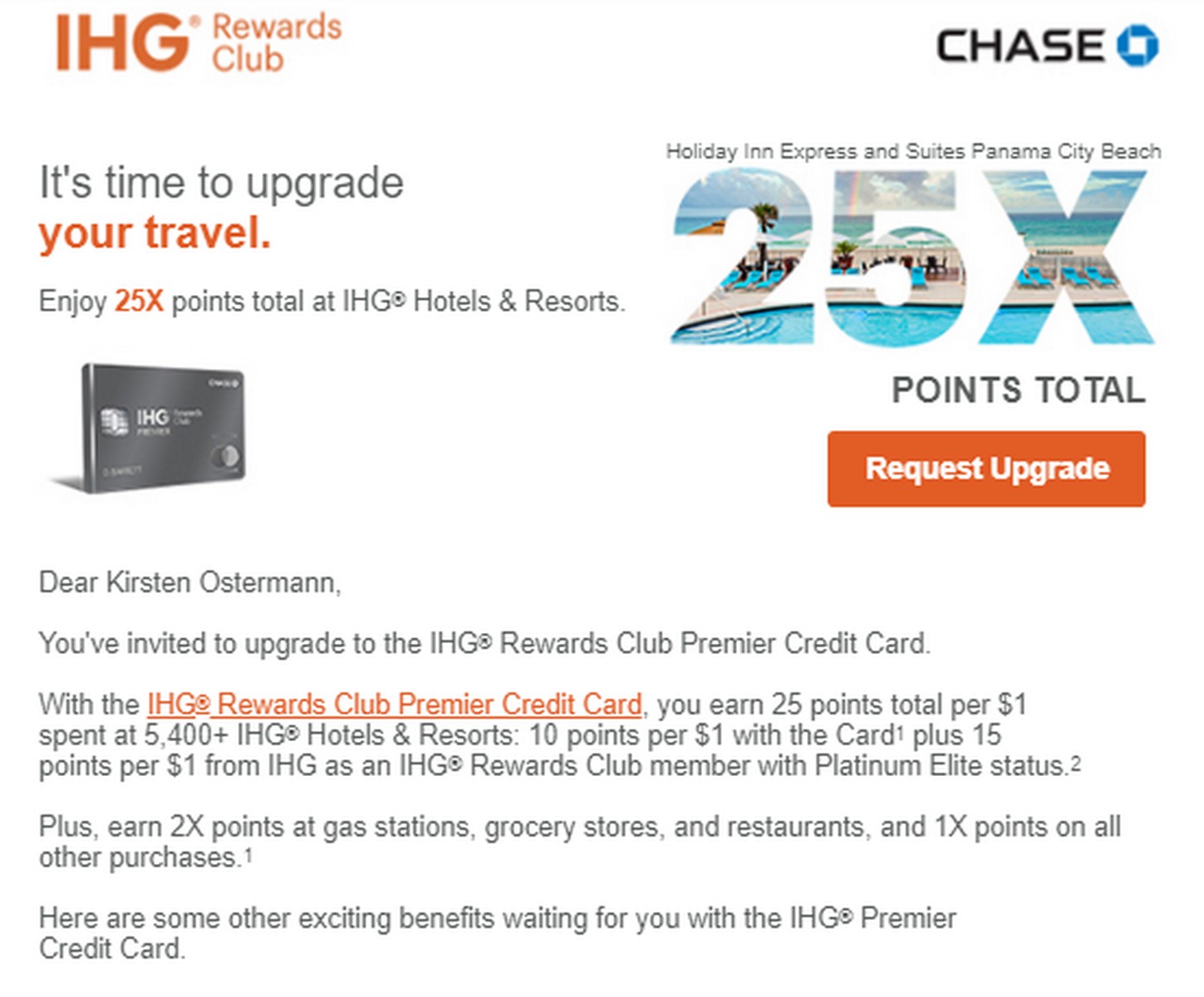

IHG Premier Upgrade Offer

As bad as the ThankYou Premier upgrade offer was Chase’s offer for the IHG Premier card. My wife was offered…NOTHING. Just the pleasure of holding the more expensive Premier card was her reward. I have already told you why I will NEVER upgrade our IHG Mastercard but they could have made it interesting with a competent offer.

They even tried creative marketing to get me to budge….earn 25X with the new card (but 15X of it comes from your status so…)

Guess what, I already have Platinum status with the IHG Mastercard. That means she would only be getting an extra 5X per dollar on paid stays versus the old card.

If you had a ton of paid stays with IHG, hopefully they are work stays or let’s talk about your choices, then this could make sense. But you would be better off applying for the Chase IHG Premier card outright since the perks of the two cards stack! But if you were over 5/24 status then it could make sense for you. You would need to spend over $1,333.33 every year on cash stays to make up the $40 difference in the annual fee increase.

Final Thoughts

Credit card providers want you holding the more expensive products for sure. Larger annual fees add to their bottom line. But without a proper offer to make the leap there is no reason to take them up on it. Unless you fall into one of the very limited scenarios I listed above you should give these a hard pass when they reach your inbox.

{kind=link}

I took the Preferred > Premier upgrade offer back in February, in the middle of a flurry of applications and with a maxed-out, sky-high-limit Diamond Preferred (BT and intro APR offers). They definitely weren’t about to offer me more credit, I managed to keep my low APR (lower than lowest available for new applicants), and I saved an inquiry and slot. I have since converted my Diamond Preferred to a Rewards+ (and paid it off). As far as I can tell, it gets the same spending offers as the Preferred used to, you just have to not use it. I’ve seen 5%/5X spending offers on the following accounts:

– My Preferred, before conversion to Premier (zero use)

– My Rewards+, after conversion from Diamond Preferred and full payoff (zero use since)

– My wife’s Diamond Preferred, which also has a small BT (so not maxed out, but still zero use)

I’ve never seen a 10X offer on any of our accounts, and I had the Preferred for 6 years.

Did you do the upgrade to unlock your ThankYou points or because you liked the earning structure on the Premier?

Uhh… it’s complicated:

I liked the earning structure and travel protections. I didn’t have anything that earned more than about 3.0-3.5% on gas or travel, didn’t want a “premium” card, and the CSP earns less (assuming 1.5cpp), so the Premier was the best fit for me. I also didn’t have any upcoming travel for which points/miles were a good option, so I could delay my next card opening (and SUB) for a while. Finally, I was just about to book $7k worth of travel, of which $4k was for others (who would reimburse me) that the Premier’s protections would cover but other cards’ wouldn’t (they’re family, but not “close family”). Between those point earnings, earnings on gas, and my wife’s Rewards+ SUB, we also covered a rental car and few nights’ hotel for an upcoming trip – at effectively 1.4cpp, it’s fine for small redemptions.

It was set to become my go-to travel card, until they announced the drop in benefits. Needless to say, I’m happy to have saved the $95 annual fee, and very happy to have saved a slot to fill with …a CSP (same SUB, ongoing protections) in the very near future. Never thought I’d even consider Chase, but the net earnings by adding the CSP/CFU combo to my wallet are just below the Premier, and the travel protections – worse before but now better – are worth that.

Dropping the travel protections is a really dumb move on Citi’s part and I think quite a few people will dump their cards because of it or at least stop putting travel spend on them.

Today I got a Chase Hyatt upgrade offer…5k points. No thanks. The extra qualifying days on the new card are the only things that might get me excited about a switch, but I travel so rarely anymore that it’s just not worth a change to pay $20 more on the annual fee.

If you think you could put $15,000 a year on the card for the Cat 1-4 free night then I would do the upgrade but if not you are better off keeping the cheaper card since you get the anniversary night for $20 less.