How Airline Frequent Flyer Programs Work

Airline frequent flyer programs have always been a bit of a mystery as far as the financial details go. These programs started way back in the late 1970’s and have evolved tremendously since then.

American Airlines was the first long-haul carrier to start such a program. Then they revolutionized it in the early 1980s by offering miles for partners such as Hertz. That meant they they could sell their miles for a fixed price. In 1987 they partnered with Citi to offer the first co-branded credit card as well.

Exact details of the pricing have been a closely guarded secret. However, last year customers got a rare look at how these programs work. And what we saw is that airlines don’t really make money by flying passengers anymore, but instead they act more like banks. They control the supply of their own currency. The video linked in this article has some great information on some of the inner working of these programs.

Financial information was revealed during the early days of the pandemic. That’s when travel demand was almost non existent and the number of passengers willing to fly was at an all time low. So airlines were all of a sudden short on cash and on the brink of bankruptcy.

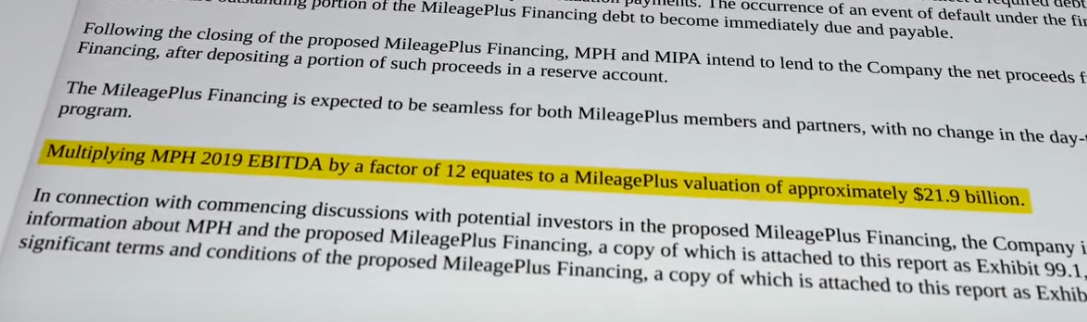

So many of the major domestic carriers started looking for loans. United Airlines for example sought a $5 billion loan and they needed to put collateral. But instead of offering part of the company, they instead put up MileagePlus Holdings LLC as collateral. That’s United loyalty program.

But since United Airlines is a publicly traded company, so they had to reveal many details including the value of the MileagePlus program. And based on one of those filings, MileagePlus Holdings was assigned a value of $21.9 billion.

Delta and American Airlines also revealed similar information about their loyalty programs, valuing them at $26 billion and $19.5-$31.5 billion respectively.

If you think those valuations are insanely high, you are probably right. The value of the loyalty program alone, which are owned by the airlines, are way more than the airline’s market cap. For American Airlines almost 5 times as much.

That means that the loyalty program is actually the only thing of value an airline has. And that was actually true even before the pandemic. American Airlines for example lost $0.50 on every passenger in 2018. But they still managed to turn in almost $2 billion in pre-tax profits thanks to more than $4 billion in revenue from the AAdvantage program.

And that is why you will see advertisement and sales pitches for co-brand cards, frequent flyer programs and elite status everywhere. Because that’s actually the most profitable part of an airline, and not because they actually care about loyalty.

Airlines have also been tweaking their programs over the last decade to maximize profits. Earning miles on flights is now revenue based, and on the redemption side we now have dynamic pricing which align the price in miles to the cash price. That leaves fewer loopholes for passengers to get outsized value when earning or redeeming miles.

Check out the video below:

{kind=link}

The flip side is the average person should not become a member of the FF programs. They will never get back their money’s worth.

What ends up as outsize profits for the loyalty program has to come from somewhere, guess where it is coming from? Frankly airlines should give the traveler an option between say an extra meal or gift on landing Vs FF miles in an established loyalty program. Very few travelers make outsized value redemptions, most end up losing.