Note: I have no direct business relationship with Chase and this post contains my educated opinion on the subject matter. I don’t have any inside knowledge or any working relationship with the bank.

Chase Made the Right Business Decision

I’m sure some of you saw that title and clicked through just to come and yell at me. If you apply for cards multiple times then Chase has sort of kicked you aside. They have told some of you that they don’t want your business. That is personal and it hurts, but it is a great business decision.

Up until recently Chase didn’t publish the official rules for getting a bonus again. Many reports confirmed that it was about 2 years, however there wasn’t anything firm in writing. Then Chase decided to publish their current rules. Those rules are:

This new cardmember bonus offer is not available to either (i) current cardmembers of this consumer credit card, or (ii) previous cardmembers of this consumer credit card who received a new cardmember bonus for this consumer credit card within the last 24 months.

And guess what. Those rules make perfect sense. Lets say a consumer got the Sapphire Preferred card, but decided to cancel after the first year. Maybe a couple of years later that person is ready to give Chase a try. Maybe it is a commercial that draws them back in or they think about how nice it felt to hold that shiny blue metal card in their hand. Either way, Chase wants that customer to come back and they are willing to pay for that.

The Credit Card Churner Is Different

Of course miles & points hobbyists see those rules differently. We immediately pick apart the words and start to formulate a strategy. If I apply for a Sapphire Preferred now, I can then downgrade it to a Freedom in a year and then get another Sapphire in month 25. Rinse, repeat. I even wrote about the best strategy to do this with Chase hotel cards.

Well guess what. Chase caught on and was forced to make a decision. Either they change the published rules and risk losing out on that customer they want to bring back or they enact other more stricter rules internally. That is exactly what happened.

For those who don’t know, Chase’s new rules are pretty simple. If you have opened 5 or more new accounts within the past two years, they will not approve you for an Ultimate Rewards earning credit card. (Freedom, Sapphire Preferred, Ink.) Some people have claimed to have been approved, but I have heard from over a dozen readers in the past month who have been denied in exactly the same way. This is real.

It’s Not You, It’s Them

So as a “churner” you might feel angry that Chase doesn’t want your business. Many of you will claim to never do business with Chase, but that simply isn’t true in most cases. Do you know why? To put it quite simply, their cards provide value.

There is a reason everyone talks about these cards on Flyertalk and in the blogs. While Sapphire Preferred may be overrated, Freedom is fantastic and we all need at least one of their premium cards to unlock transfers to their travel partners such as Hyatt and United. This is value.

A Change of Strategy

What are you going to do now that you know Chase won’t approve you for any new cards? Frequent Miler pointed out the change in his strategy yesterday. Just a few weeks ago he wrote about the optimal way to earn Ultimate Rewards through strategic applications. Now instead of cancelling and getting the bonus again, he has to keep a premium card long term.

Do you see what Chase did? By instituting these rules they forced him, me and you to keep their cards. To pay an annual fee and use the cards as intended. Since we now know they won’t approve us for more bonuses, we have to become the valuable customers that Chase wants. I’m sure as heck not giving up my Ink Plus, because if I did, then I don’t know that I would be able to get it back.

Of course we are still pretty savvy and we will ask for retention bonuses and otherwise find efficient ways to keep this relationship going. Chase is alright with that. They would rather operate within the new guidelines then give us bonus after bonus after bonus. They sort of have us where they want us and know that we would be stupid to walk away.

Co-branded Cards

Update: Chase is most likely instituting the 5/24 rule for co-branded cards in April, 2016.

Chase also has one of the best assortment of co-branded travel cards and guess what, churners are somewhat welcome to apply for those. Chase has contracts with these partners to deliver a certain number of approvals and that may be why they haven’t cracked down as hard on co-branded card approvals.

That isn’t to say they haven’t cracked down at all. Some people have reported being denied lately for too many applications and too many new accounts. Overall co-branded cards are a churners best route to a good relationship with Chase, however don’t expect them to give you card after card anymore. That would be a bad business decision.

Things Change

Chase is sort of at the top of the credit card food chain right now. Their business strategy coming out of the “Great Recession” was the correct one and they stole a ton of market share on both the high-end and low-end. Chase is dominate in the market and thus can get away with things like this. Of course that has not always been the case and most likely won’t always be.

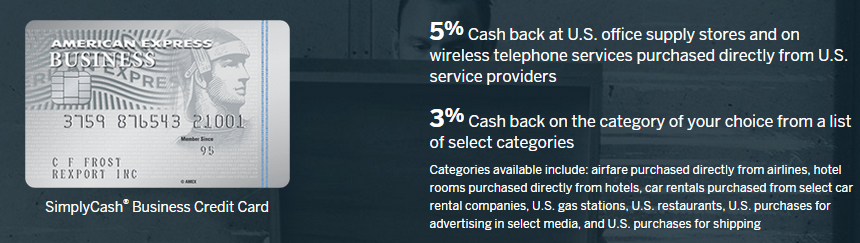

We have seen aggressive moves from just about every bank over the past couple of years. American Express is desperately trying to grab business accounts with huge bonuses on their Gold & Platinum products and they have been pushing their SimplyCash Business card as a competitor to Ink. If Chase won’t approve you for an Ink, guess where you are most likely to go?

What this means is that today’s good business decision may not be the right move down the line. At some point Chase may need to start bringing up their numbers on the Ink or Sapphire and guess who they can rely on to be there waiting? By that time of course all of us will should be eligible for new bonuses on those products under the published rules.

Conclusion

If you look at this situation from Chase’s perspective then you will see why they made this decision. Fortunately for us the market dictates a lot of what goes on and that simple fact will most likely keep other banks from following suit. We may see an overall crackdown, but as soon as a VP needs a bonus, we will see the Citi AAdvantage Executive deal all over again.

At this point I am slowing down and enjoying my Chase cards. I’ll definitely keep an Ink Plus/Bold and downgrade my Sapphire to another Freedom. Then I’ll just sit and wait. If/when Chase needs me to boost their numbers, maybe just maybe I’ll consider applying, but only if they beg. 😉

{kind=link}

Damnit!

How come I missed this heated discussion! Dude! All the TMZ good crap comes out during these reddit hater posts..

THIS IS SPARTA!!

Anyway, Shawn is honest and Solid Snake about his posts dude. I totally back him up. Cant say the same for a few other bloggers, but like he said, everyone is entitled to their own Yelp reviews.

Trust me, I know the new Chase rules suck big black coc. I can also easily hate on bloggers and churners and MSers who “break” the system and close up good deals. I mean look at how quickly some deals die and I am still bitter about the axe on REDBird CC load!! Not to mention stupid incompetent people keep breaking the Walmart MoneyCenter machine when they try to load over $2k in 10 min! Like dude! Respect your comrades man!

But there will always be Axis and Allies in this game and we just gotta support the awesome honest ones who help those in need. Thats why I really like this post that details out the current landscape of Chase. I really dont know wtf people are arguing about or hating on. You dont see no affiliate links and shit on this post do you?

Also, I find it ridiculous to hear some churners feel angry that Chase doesn’t want their business. Uh, yea… they dont. Their credits cards werent made for you to game the system. What are you upset about??

Or some will claim to never do business with Chase. Again, uhh why? cuz they dont like you gaming the system so its their bad??

Of course, theres splash damage and innocent wives and children get killed in the crossfire. Its part of war. It sux.

But just so everyone knows, large financial institutions such as JPM Chase are not just looking to kill churners. There are many other factors at play so dont just think its all about points/miles game. Thats part of the reason for sure. Specifically for JPM Chase, they were just fined $136 million for illegal debt collection practices on CC crap. That was only the recent one. It was raped up the butt from previous years as well.

http://trib.in/1eHf4Oi

So what does this mean? It means they cant just hand out credit cards to any dildo and increase their credit risk exposure and default collections. Again, we are talking about losers here and not responsible readers like you, but there will always be collateral damage and civilians get killed all the time.

Good luck to us.

THIS IS SPARTA!!

Question about the 2-year rule: If I had Chase Saphire Preferred and downgraded to the non-annual fee version 2 years ago, am I eligible to apply for the Preferred again?

You would be eligible for the bonus, but you may not be approved if you have opened 5 or more cards at any bank over the past two years.

Can you expand on this comment: “I’m sure as heck not giving up my Ink Plus, because if I did, then I don’t know that I would be able to get it back”?

I’ve got a bold and a plus fee coming up, along with my CSP, and I’m having trouble justifying paying for the Ink cards when there’s a no-fee Ink Cash card out there that I could just transfer to my CSP account.

I just want to make sure I’m not missing some reason that makes the ink “un-cancellable”.

Thanks!

Just that they probably wouldn’t approve me for a new one. In my view it is best to keep an Ink Bold/Plus for UR transfers and downgrade a CSP to a Freedom. In your case it sounds like you value the CSP more, which is perfectly fine. The only really important thing is to keep at least one premium card for transfers.

Thanks Shawn. I guess I do value the CSP a bit more. Mainly b/c I like the fact that in the instances where I need to get Chase on the phone I’ve got a phone number on the card that gets me directly to a human being.

Also, because the Ink Cash does everything the Plus/Bold does (I believe that’s correct, please let me know it it’s not) except with $25K limit at Office Supply/Cell Phone/Satellite/etc… instead of $50K (neither of which do I even get close to) then it seems a logical choice to downgrade the Bold/Plus and keep the CSP. Also, I already have a Freedom.

Thanks again Shawn, this helped.

shawn, first of all, that official rule contained in the Freedom bonus disclaimer does NOT reflect the important reality that Chase will decline most applicants who have had 5 or more accounts opened (INCLUDING AUs) with ANY BANK in 24 months.

Second, Chase has thrown the baby with the bath water, so to speak. We’ve maintained our Freedom and Ink family of cards and paid our annual fees for years. Never have asked for a retention bonus. I never had a Freedom card, only as AU to my spouse’s. Got declined due to this looney 5/24 policy.

In implementing this unofficial but much-repeated (by Chase recon reps themselves) 5/24 policy, they may have closed the loop for churning cc bonuses and yes, perhaps I will keep my cc’s with them but I GUARANTEE YOU, that I will not keep my personal and business bank accounts with them any longer.

Even after our branch rep had filed a special recon on my behalf due to our long-term relationship with the branch (since it was WAMU) and significant balances in our bank accounts, Chase did not reconsider, to the frustration of our bank rep. It’s as if Chase has said to me, we want your money in our bank but we won’t give you the piddy Chase Freedom. Ok then, I will take my money elsewhere

First off, I mentioned the new rules, so I’m not sure if you read the whole article. Secondly, I agree there will be some negative blowback from this, but in the end Chase has made a business decision that will help them retain the customers they want without taking on new cardholders they don’t. I don’t like it either.

Also, as I said I think market conditions will eventually change and at some point Chase will need more signups. When that happens all of this might just go away.

from a business standpoint you are brown-nosing…While it is within Chases rights to make up new rules, what’s next?…”i’m sorry Mr. Smith, we cant give you a credit card because our records show that you pay your bill every month and we make no interest money off you”….the fact that chase has over a dozen cards and sends out offers all the time, and then penalizes you for having too many apps or accepting too many offers, is hypocritical …to base acceptance on anything but your credit score is discrimination…if they don’t want people signing up for bonuses, then they should stop offering them, or do like Amex did, and limit them to once per product, period….to refuse their products to consumers that have applied for more than 5 cards in 2 years all the while sending out offers for their 20+ varieties of cards is wrong on many levels….my advise is to cancel every chase card when its annual fee comes up and when they ask the reason, tell them you don’t want to have too many cards for chases liking.

Not brown nosing. I’m just analyzing using my background in business and finance. Again, there are a ton of things in this post that Chase would hate. This is definitely not written to pander to them.

@ Will, this really made me chuckle.

It’s not like Chase to ignore an SM. They probably haven’t gotten it or lost it or whatever. I’m sure if your friend writes them again, they will send her a polite, canned, and completely meaningless response.

Because Chase will never admit in writing that this is their new policy. They change policies all the time. The reason why this hobby exists is because we take time to EMPIRICALLY analyze and dissect what’s going on, not because credit cards tell us what they allow us to do and what they don’t.

In conclusion, please understand that Chase doesn’t know Shawn any better than they know you or me. Chase might know Gary, Rick, and Lucky and maybe–maybe–a couple of others (no offense, Shawn), but no, I’m pretty confident that Shawn doesn’t have a reason to be nice to Chase. 🙂

Bad move Shawn. You’re feeding the sharks who butter your bread.

This chase move doesn’t just hurt you and your churner buddies, and yes, you’re already adjusting strategy for YOU. Yet you’re belittling and ignoring we non-churners, we little folks, and our business that chase will lose as a direct result of this change.

Special friend of mine had carefully been building good credit — so good that her scores are close to 850 (sic). Yes, in the past 18 months, her careful, prudent, responsible, NON-CHURNING strategy has included the opening of exactly five cards — including four of the Chase travel co-branded cards. (She’s had the Chase Freedom card for over a decade…. it WAS her top card as she raised a family, going back to when the categories were stable…. )

But she also was looking forward to adding her own Sapphire or Ink cards this fall….. No longer. She wrote to chase for clarification as to just what the new policy is, if she’ll automatically be refused and declined. Chase ignored her secure message.

If Chase arrogantly doesn’t want her business, she won’t even bother applying and waste the hard-pull on the near perfect credit. Instead, she’ll take her business elsewhere — AND reconsider previous thinking to keep even the IHG and Hyatt cards for the long haul.

Yes, you have a business to run. You need chase to do business with you. You need to be nice to them, to be “understanding.” I’d have expected this from Daraius…. But from you? oh yes, you chortle, your title was click bait, you wanted us to read it (thus improving your click count for your advertisers)….

And so it goes. Your true “loyalties” exposed….. and you’re proud of it. Good for you.

Hey Will,

Thanks for your response. Everyone is entitled to their own opinion, but your comment is pretty ridiculous. I hope you know that.

First off, lets start with the intro. Did you not notice when I said I don’t have a direct relationship with Chase? As in I don’t know anyone or talk to anyone at Chase.

Secondly which parts of this post do you think Chase would like? Do you think they like when I call Sapphire Preferred overrated? Do you think they like me using the term churning and exposing new people to the practice? How about where I talk about the Amex SimplyCash card as an alternative to Ink?

The truth is I am pretty sure if Chase even knew who I was (no offense taken Andy) then there are many parts of this post that they would hate. I’m also pretty sure they wouldn’t like the part about me being in line to apply again once the rules are changed back. Not to mention the post I linked to about Hacking Chase Hotel Cards.

In truth, there are thousands of posts on this website that show I have no loyalty to Chase or any bank for that matter. I am always as honest as possible and if Chase had anything to do with this post it would be disclosed up top. Instead, you see the exact opposite.

Finally, you call this headline clickbait? How is that? It mentions Chase’s new churning rules and how they are a good business decision. So basically my title accurately represents exactly what is in this post. I don’t know how to write a more accurate headline. If I wanted to write a clickbait headline it would be something like this, “How Chase’s Bold New Policy Change Will Cost You Thousands of Points!”

Everyone is entitled to their opinion and so are you. I am sorry your friend is having issues, but it sounds like she wants to get her 5th Chase card in two years. That is more than normal people. I hate Chase’s new policy as much as her. My goal is to show my readers the truth about what is happening based on my experience. If you don’t find value in that then please feel free to unsubscribe. I value every reader, but it is obvious that you don’t feel I am sincere. That simply isn’t true, but you are definitely allowed to have that opinion.

Have a wonderful night.

Damn, nice response.

lol, churners created this problem for regular people really, but it’s the Chase’s fault?

I don’t know they sort of picked a bad time to do this since Citi is making itself so attractive with the Premier and Prestige, maybe I won’t miss Chase.

I think this is a well written, honest assessment of where Chase is coming from and where we fit into their business model. The value here goes both ways though, and fortunately for us – the churners – we live in a capitalistic society and we have other options and credit card issuers hungry to gain new business.

Couple of quick thoughts though. First, I’ll be churning my bank bonus again with Chase next year (I wasn’t planning on closing the account after the 6mo requirement). I had adopted a philosophy of avoiding MS activities with Chase (other than for sign up bonuses) but I see no value here anymore regarding a banking relationship.

We rarely fly as my wife won’t leave the ground so partner transfer value is lower for me than your average MS’er. The only value I personally place on the points is in transferring to Hyatt. I have about 200,000 in points right now and about 8 months before my CSP AF is due. I may transfer my points by then to Hyatt (including a few vacations over the next year and book them) and close my CSP and simply redeem my points for statement credit.

Speaking of the hunger of other CC companies wanting our business, I hear Discover is offering some good value lately 🙂

Great article.

But in my case Chase lost a customer. I was going to keep my Chase Freedom long term. But since I got denied for one of their co branded HYatt credit card and I know I won’t get approved for a UR credit card that allows transfers I canceled my freedom. I planned to signed up for the sapphire preferred at the end of the year so the 60k points I’ve earned in my freedom could be transferred to Hyatt. But now that won’t happen. So that’s that. Only keeping my Amazon my only chase card because it’s one of my oldest.

I just have to maximize my Amex everyday preferred and gold card.

agreed. I will Keep my freedom and my legacy sapphire (no AF card), but will be cancelling the SPG once my year is up. along with my Marriott for business and My traditional Marriott. For me, they are losing at least two if not three Annual fee cards. With some great AMEX offers around lately, most of that spend is shifting to AMEX for me.

So they may not care about $200 in annual fees, but they will care about the $20,000 in swipes I do on those cards.

Why would any of this cause you to cancel the SPG?

You should keep the freedom, since it doesn’t have an anual fee. These rules will likely change at some point, and there isn’t a downside for you to keep it. Just don’t use it.

5 or more Chase accounts or just 5 new accounts from anywhere?

5 or more accounts across all banks.

Do you think having a JPMorgan Private Bank account can influence the 5/24 rule?