Chase Credit Cards

I’ve asked myself the above question here and there over the years. I generally end up shrugging, knowing that I can still accomplish worthy goals with Chase credit cards regardless of how lame the bank is. But occasionally, I feel it’s worth reminding myself, and you, dear reader, about certain points and travel hobby pitfalls. Today is one such day, and once again, Chase deservedly draws my ire.

Obfuscation Continues

Chase routinely obscures the rewards picture for cardholders. Sometimes that’s obvious over time, such as with the Chase Sapphire Reserve (more on that in a bit). Elsewhere, Chase has made smaller-but-still-annoying changes.

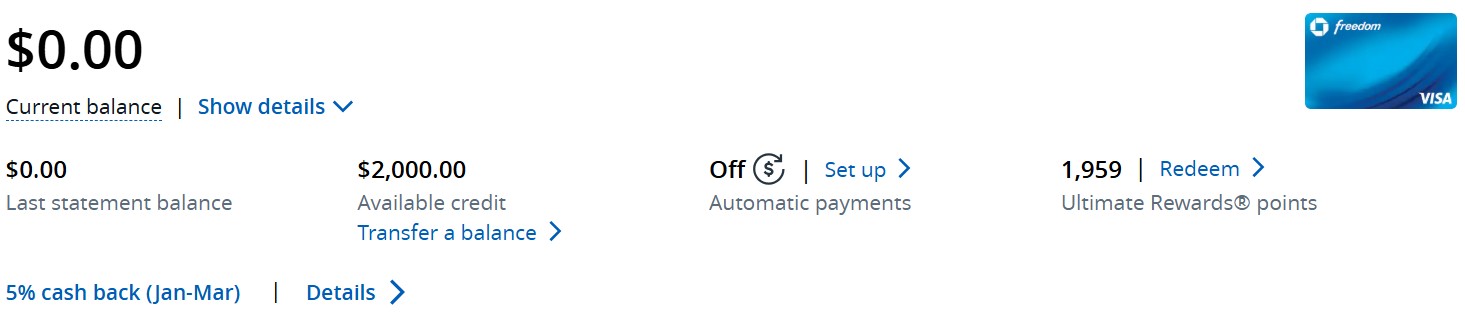

In my view, Chase’s website isn’t any better than it previously was. Rather, it’s become more unhelpful. For instance, I recall years of being able to fairly-quickly discern if I had activated my Freedom cards’ quarterly 5%/5x categories. After logging into the Chase site and clicking on a given Freedom card, I could quickly see the word “Activated” and know I was good to go for the existing quarter. Now, look how Chase unhelpfully updated the site:

Chase has removed “Activated” and replaced it “Details.” This requires two additional clicks – one on Details, the next on the particular card I want to review – and scrolling to see whether the Freedom activation occurred. Oddly, I don’t need to scroll to see the status on my Freedom Flex accounts. Apparently, things need to look considerably different on the “regular” Freedom and Freedom Flex pages. But hey, while that bothers me, it might not annoy you. Try this next one.

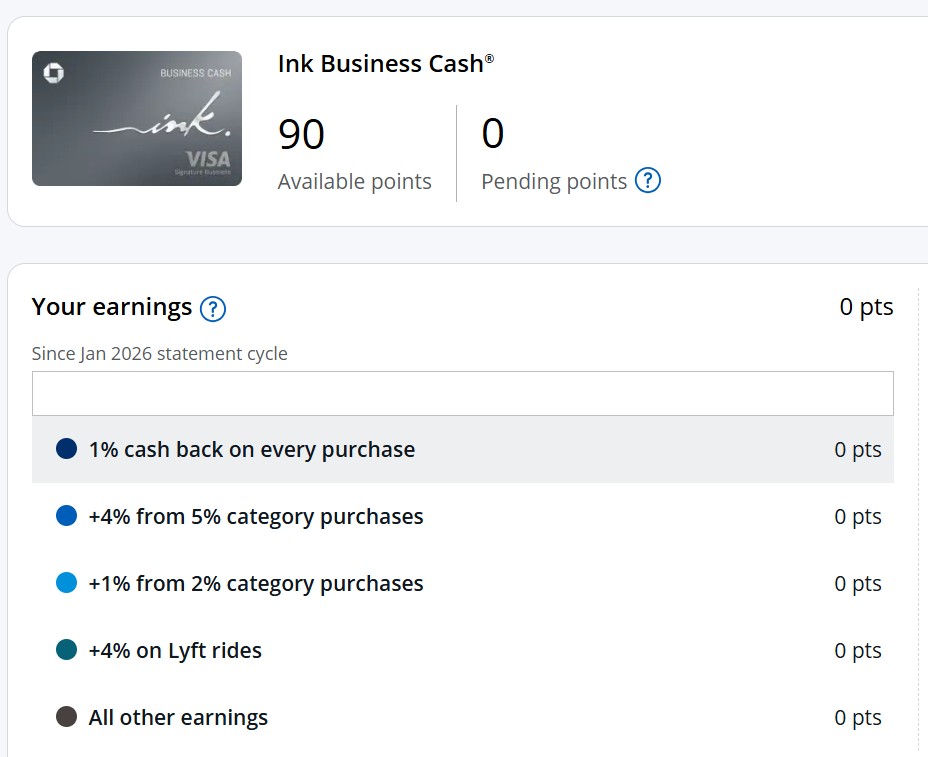

As you may or may not know by now, determining one’s Chase Ink Business Cash 5%/5x spending status is harder (or impossible) to identify online. Previously, the timeframe displayed would start at the beginning of the current cardmember year period. Now, it looks like this:

This info is essentially no help for 5%/5x purposes since it only covers the period since the beginning of the calendar year. Those not paying close attention may think they have fresh capacity for those categories, while in reality they spent in them during the previous calendar year/within the same cardmember year. At best, this isn’t a thoughtful update by Chase. At worst, it looks like the bank’s encouraging cardholder mistakes. Of course, other methods can be used to determine your 5%/5x status, such as reviewing statements or calling in to confirm your cardmember year. Regardless, it’s not as easy as it used to be.

Less of a Good Thing

Chase Freedom

The Chase Freedom and Freedom Flex have provided a relatively simple option for obtaining 5%/5x in categories rotating every quarter, up to $1,500 in spend. Such options have generally included staple categories and others which are still fairly broad and reasonable. But it seems like Chase is increasingly hemming us in.

- 2025 Q1: Grocery stores (excluding Walmart/Target), fitness clubs/gym memberships, hair/nails/spa services, and Norwegian Cruise Line, Tax Preparation/Insurance (Mar only)

- 2025 Q2: Amazon, select streaming services, and internet/cable/phone services (Jun only)

- 2025 Q3: Gas/EV, Live Entertainment, and Instacart

- 2025 Q4: Chase Travel, Department Stores, Old Navy, and PayPal (Dec only)

- 2026 Q1: Dining, Norwegian Cruise Line, American Heart Association

In my view, these categories are tougher to responsibly earn in. Significantly spending in these categories increasingly involves expenses incompatible with the way many of us normally live. Now, I’ll move to the redemption side.

Chase Sapphire Reserve Pay Yourself Back

Chase Pay Yourself Back debuted in spring 2020, and I was a big fan for many years until recently. I could effectively cash out Ultimate Rewards points at 1.5 cents or 1.25 cents per point when I was previously doing so at 1 cpp. Chase has limited 1.5 cpp max value to mostly 1.25 these days. The categories have tightened up over time, also. In the current quarter, cardholders can redeem in the following three categories at 1.25 cpp, the fourth at 1.5 cpp:

- Gas stations

- Fitness Clubs/Gym Memberships

- Annual Fee

- Select Charities

Theoretically, someone can more significantly redeem at gas stations by purchasing gift cards and applying points via Pay Yourself Back. But of course, many cardholders aren’t necessarily comfortable with such purchases. And historically, I’m accustomed to seeing broader categories here, as well. Other Chase credit cards participate in Pay Yourself Back, but the Sapphire Reserve has generally had the best categories. Sadly, I expect they will keep getting worse for the Reserve.

Chase Band-Aids a Compound Fracture

Early on in the latest round of premium card refreshes, I felt Chase had already won in the court of public opinion. But Amex came back in a big way, essentially how I’d hoped. Meanwhile, Chase Sapphire Reserve negatives became more prominent. It seems that Chase designed the card to discourage people dumping it, but it apparently had the opposite effect for some. That was definitely the case for me. I also pondered if Chase was sweating the Sapphire Reserve. Elevated card welcome offers appeared and lasted longer than I expected. The bank added a temporary travel credit that I perceived as a Band-Aid to the card’s bigger problems.

We’ll see where things go from here, but I’m even less inclined to return to the Reserve now than I was before.

The Obvious One

What hangs over everything is that Chase still employs what I consider the most draconian of all credit card application rules – 5/24. This rule is why my wife and I gave up on ever obtaining more Chase credit cards via new application. Beyond our existing Chase portfolio, we assessed that we could obviously do better taking our business elsewhere. So many other individuals have come to the same conclusion, but this rule is continuing to work on others. I occasionally speak with individuals who are avoiding cards with other banks because they are waiting to hopefully pick up another Chase product. If they haven’t done so already, I encourage them to consider if waiting around for more Chase cards is the best personal decision.

Chase has essentially outsourced some of their marketing to cardholders, and even non-customers just hoping to get one someday. While that may be diabolically genius, I also find it uncool.

Chase Credit Cards – Conclusion

Again, I’ll keep finding the wins where I can with Chase, but they seem fewer and farther between these days. Regardless, it’s taking customers more work to do so, which I expect Chase wants. Those wins will take a relatively-limited amount of my time, though. I’ll continue to focus my efforts more on Amex and elsewhere, as I’ve done for years. All those other banks not named Chase have won the war for my attention span long ago. Maybe they should for yours, too.

What annoys you most about Chase these days?

{kind=link}

They spelled it wrong… its now quarterly bogus categories.

😉

With a combined total of 16 biz and personal Chase cards…my wife and I have become less and less fans of Chase.

The necessity to call customer service to get them to Combine Points is loathesome.

As mentioned in the article, the challenges with the website not just limited to the Freedom card but it is a good start.

Why is it so difficult to put a link to what are the bonus categories for the quarter?

Hyatt transfers use our URs. The rest of the cards have a place but they are getting squeezed by other bank cards with better value.

The Reserve card took a massive nosedive in value. Increasing the annual fee to $800 while dropping the 1.5cpp portal redemption was the nail in the coffin for me. All the coupon clipping isn’t worth it. I will be downgrading soon.

Hello,

I do not like how they seem to control everything. The just out of the blue changed my freedom to a freedom flex. So I quickly appllied for a flex so I wouldn’t miss out on the bonus. Luckly I was under 5/24 but was that the best use of a card slot? Their point system does seem to work for me best. I am able to use my old Ink Plus card for a lot of transfers. It seems to work the best for me in use of flight points. I’m not a big player but for my system they work. I just don’t know how I could use all the Amex credits on the platinum and still get value from it. I loved the article and your articles and the perspectives you give. I agree with all your positions in this article. Hate the new navigation of the site.

Tip of the iceberg. Chase has so many other negatives. Just one minor, but recent, example related to this was my recent experience with a hotel booked via Chase points. I booked a hotel with 60,000 points at 1.5x. Not a great deal, but it worked for me in this situation. The hotel has lowered the price on the date I needed. I looked at cancelling the reservation and rebooking it. Chase will refund the 60,000 points but also make them worth 1x when I go to use them, negating the price drop. This problem doesn’t even include their small print that says it can take weeks to redeposit my points, in 2026 does it take weeks to do such a thing?

The website will not let me into my own account. It keeps giving me a message to call chase cust seervice. I have calle them and after wasting an hour on the phone with them, they get me in. The next time i try to log in the same thing happens !

Interesting. I find the Chase website to be the best of the bunch. I still get value from transferring to Southwest, and on Reserve, the 4X on hotels and dining and 3X on dining is compelling to have on one card. True, I wish they’d kept the broader travel category for 3X, but I’ve kept the Ink Preferred for those situations. I still think Amex has the best offers, but generally speaking, the Chase ecosystem still wins the day for me. Late last year I got a discount on a new iPhone through their partnership with Apple. I’m sure others will say there are dozens of other ways I could have redeemed points, but this is the arrangement that works best for my use case situation. The only disruption to this is the Bilt card, and I’m still waiting to see just how beneficial the Palladium will be after Year 1, maybe Year 2 after my daycare expenses cease, hopefully…

Fair enough, Joe. Thanks for reading!

Chase UR has definitely lost some luster

My personal tier 1 transferable points ecosystems are Chase UR, Citi TY and Bilt

Remember what Mae West said about whistling.

The first challenge with Chase’s ecosystem is its transfer partners. Compared to other card issuers, the breadth is limited. Then, compared to others, earn rates are meh. For Slaves Of Hyatt, Bilt offers 2x/3x earning on ordinary spending and the ability to channel Rakuten points. To me, Chase has lost relevance as an ecosystem. With SUB restrictions now in place, I don’t understand why people still obsess about 5/24.

Your headline is both eloquent and elegant. Well done. /s