When Should I Pay My Credit Card Bill? Best Tips For Your Credit Score

“Before it’s due” is the usual first answer to when you should pay your credit card bill. However, there’s more to it. If you’re interested in boosting your credit score, read on. Here’s a look at paying your credit card bill in a slightly different way, in order to help your credit score go up and stay there.

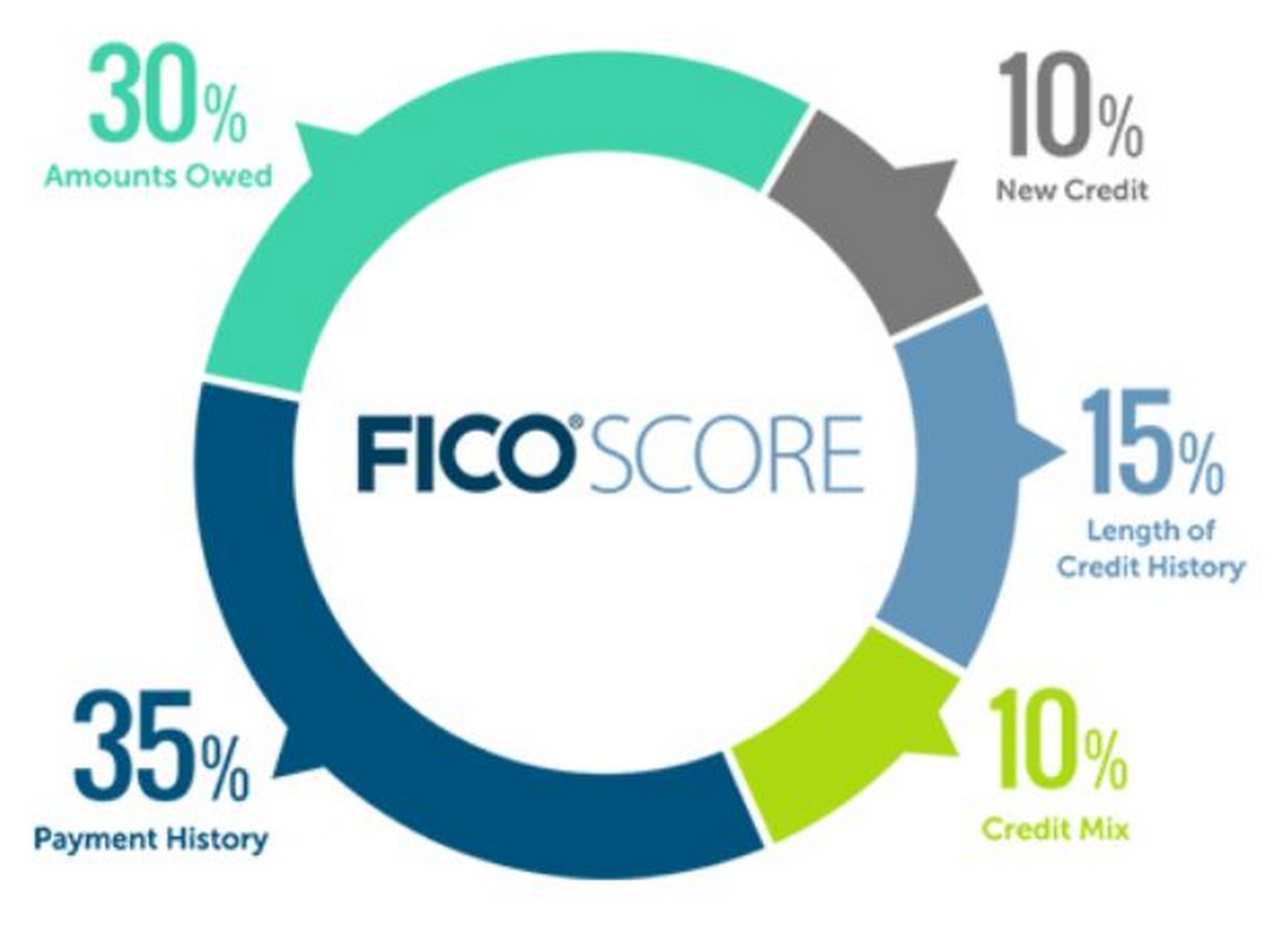

How Your Credit Score Is Calculated

We’ve talked about this in our beginners’ series here. Your credit score is counted like the image above. Paying your bill on time, “by the due date”, accounts for 35% of your score. You meet that requirement even if you make that $35 “minimum due” payment on a bill of $3,000. Not the best for your finances, but it checks the box here.

The other factor at play with paying your credit card bill is the section “amounts owed”, which is 30% of your score. This is what we’re digging into today.

When Should I Pay My Credit Card Bill? 2 Options

I want to look at 2 options here. The first will be the standard answer. After that, we’ll look at a better option.

1 – By The Due Date

Yes, this is obvious. If the bill comes and says “Pay by June 10,” you should pay by then. Even if it’s the minimum, make a payment by that date. This payment method focuses simply on receiving your bill and paying it.

Remember that a full 30% of your score is based on “amounts owed”. Think about all of that holiday shopping you do in November and December. Your credit card bills are probably higher than normal. That means your “amounts owed” is up, and your score probably goes down around this time of the year. You can check your score on Credit Karma or AnnualCreditReport.com to see the history for fluctuations in your score when the bill is high.

Since we want to boost our score, I propose a different approach.

2 – Before Statement Closing

Think of our example above where your credit card bill jumps up in November and December. You do what you normally do: use the card, get the bill, pay the bill. But what if we pay it earlier?

Assume your credit card statement closing date is the 10th of the month every month. I’ve spent a lot this month, and my bill will be high. Because of that, my score could go down. Instead of doing that “get bill, pay bill”, I can pay earlier. Pay your card before the statement closes, and keep the amount of the credit card bill lower.

If I make a $1,000 payment today, my credit card bill is only $2,000 instead of $3,000. My “amounts owed” is lower, and this benefits my credit score.

How Much Should You Pay?

There are some different opinions on this. If we consider “when I should pay my credit card bill” as right before the statement closes, there could be a drawback. Now, it looks like you aren’t using the card. There’s no activity being reported to your credit report. There’s no bill, so there’s no proof you paid later on. (I’m speaking in broad terms here)

In order to really maximize this, it’s still a good idea to let your bill have something on it. Pay it down to $1 or $25–something small. Your “amounts owed” is super low. Credit utilization (how much of your card’s limit you’re using) is super low. You look responsible. All of these things help your credit score stay high, plus you have activity generated on your credit report–another good thing, because it builds credit history (another 15% of your score).

Some people will pay their bill all the way to $0. Others pay it down to $1. Some people think “just get it low” because typically 5% or lower credit utilization is considered excellent.

When I use a card a lot during a particular month, I pay it down however much I can before the statement closes. Even if it’s not everything or not the majority, keeping the bill low helps your credit score.

Other Considerations

Of course you should pay your whole bill every month, at least by the due date. Let’s say you won’t be able to make the full payment on your bill this month for some reason. It happens. This “pay early” strategy also helps here.

The interest on your credit card is charged against the “average daily balance”. If your bill is due on the 30th, and you can’t pay all of it, you’ll be charged interest on whatever part remains unpaid.

When should you make the next payment? As early as possible. Your interest will be charged on the average daily balance from the month. If you make a payment on the 10th day of your monthly credit card cycle, you significantly lower the average daily balance. That’s true even if you aren’t paying the full balance. If you wait until the last day (day 30) to pay a card with a $2,000 balance, the average daily balance is $2,000. If you make a $500 payment on day 10, your average daily balance is $1,666.67.

When interest is calculated, you could see $60 or more in savings just on the interest the bank charges you that month. That adds up over time.

Final Thoughts

In this hobby, keeping your score high is important. It helps with approvals for future credit cards, which is the whole point. If you pay your credit card bill before the statement closing, in order to keep the bill as low as possible, you’ve moved into advanced mode. That will help your score.

{kind=link}

Once I got my credit cards paid off a couple years ago, I started paying them off when my purchases were posted. I found myself in a lot of CC debt and getting it paid off made me be REALLY aware of any amount sitting unpaid on my cards. I think in the last 2 years the most I have ever had sitting on my card for more than a few days was $200. BTW, my FICO score was 841 last month so I am not sure having that zero balance is having a negative effect on my credit score.

As a business, credit card issuers love cardholders carrying a balance and paying that interest. But, their credit analysts hate cardholders carrying a balance. So, whether one’s game is to 1) increase one’s credit limit spending flexibility or 2) periodically add to one’s stable of cards, don’t carry a balance. BUT . . .

The FICO algorithm has a skew in it. If you pay off all of your cards before the statement date so that you have $0 balances, the FICO algorithm considers that “no recent use of credit” and lowers your score. There is a small dollar balance that maximizes one’s score. That sweet spot dollar balance is different for each person. For me, it is $750 to $1150. For my wife, with the same cards, it is lower. You should experiment with this over several months. Fine tuning your number might lead to targeted offers.

Correct. As mentioned in the article, a $0 statement balance is not beneficial.

I recall reading somewhere that the look at your credit utilized etc occurs at the end of each month; and a recommendation to do a pay down like you describe before the month ends (but not necessarily tied to due date/billing cycle). Is there any basis to that?

Vince – you may be talking about when banks report information to the credit bureaus. This is typically when your statement closes, though other things can affect it (if other info needs updated, like you changed names after getting married, for example). Thus, the new info on utilization is tied to the statement closing date, which is why you could pay before statement closing to get lower utilization rate.