MTM101: Points And Miles For Beginners – Part 2: Getting Your First Card

Welcome to Part 2 of MTM101: Points And Miles for Beginners. In this post, we’ll quickly recap where we stand after part 1 and then use that as a foundation for evaluating the credit cards available today. There are literally thousands of credit cards we could apply for, so we’ll look at choosing the first credit card to apply for. We’ll compare popular cards against one another and then be ready to apply for that first credit card. Part 2 ends with you applying for that first credit card and beginning your journey to unbelievably cheap travel using points & miles to fulfill your dreams. Let’s get started.

Recap From Part 1

In part 1, we started “Points And Miles For Beginners” by understanding how this hobby works and then ended with a homework assignment. Hopefully, you’ve done these 4 things:

- Pull your free credit reports from AnnualCreditReport.com and make sure everything is correct.

- Sign up for an account on CreditKarma.com to track your information easily.

- Make a list of all credit cards you have opened in the last 2 years.

- Join our Facebook group, where you can easily get opinions and advice from our thousands of members.

if you haven’t pulled your credit report, you aren’t ready to move forward. There’s a reason that’s item #1, so please do that. It’s super important to know your current credit profile before you are ready to apply for credit cards. So, with that in hand, let’s move forward.

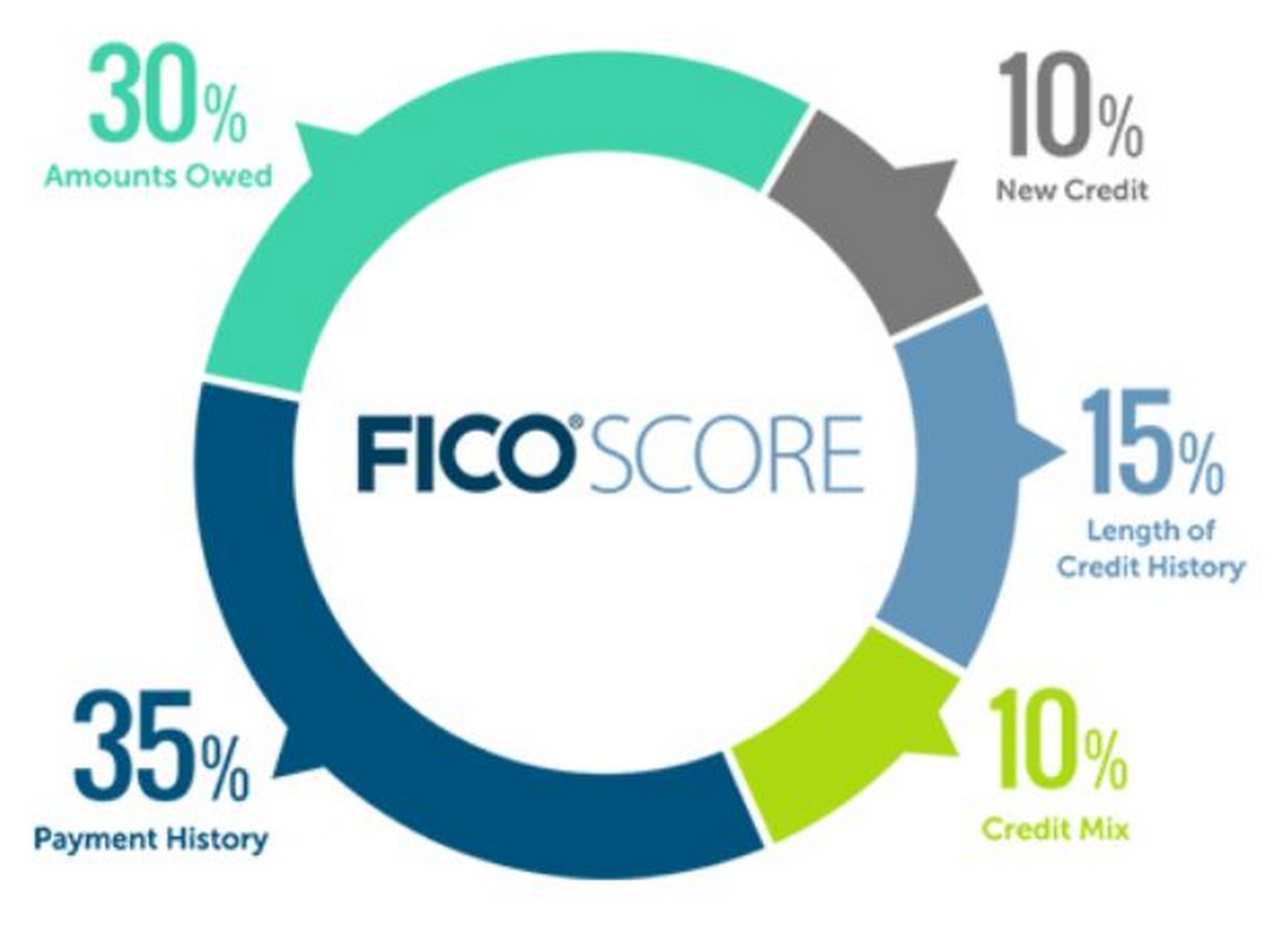

Your Current Credit Profile & Score

Now that all of the information on your credit report is updated & accurate, you should have a score. Scores range from 580-850. Higher is better, obviously. According to Experian, less than half the people in the U.S. have a score above 740, which is considered “very good” (800+ is “exceptional).

A higher credit score is built by a history of using credit responsibly, as shown in the image above. The biggest elements are keeping credit usage low (not running high balances on your card) and paying on time all the time. Banks are more likely to approve you for credit cards if you have a higher score, good history, and don’t make them worry. As you start learning about points & miles for beginners, it’s important to remember that every credit card you apply for is a business decision for the bank. “Is this person likely to pay the bill?” If they don’t think you will, you won’t get the credit card.

The 5/24 Rule

We also counted up all of the credit card accounts on your report that were opened in the last 2 years. Why did we do that? It has to do with something important to know in this hobby: the 5/24 rule. The “24” in this number is 24 months, or 2 years. The “5” refers to a limit on the number of new credit cards. Here’s how it works.

The 5/24 rule is from Chase, one of the most popular banks for credit cards in this hobby. They have a rule that they will automatically deny you for any applications if you have opened 5 or more credit cards in 24 months. 5/24, get it? And this rule applies not just to their own products. If you have 1 from Chase, 2 from Citi, 1 from Bank of America…that’s 4. If you can see it on your credit report, so can Chase, and it counts. What’s your number of new accounts in the last 24 months? For most people, it is 0 or 1. As long as your number is under 5, we’re ok with Chase.

Other banks have their own rules, which will come into play later. However, we don’t need to worry about those right now. Just know that each bank is different.

Choosing A Good Credit Card

Now that we know our x/24 number and that we are ready to apply for our first credit card, I recommend starting with a card from Chase. There are a few reasons for this.

- Chase is one of the more restrictive banks. With that 5/24 rule, once you pass it, you cannot get any credit cards from Chase. It doesn’t matter how good your credit score is or how much money you have. We should start here, since their cards will become inaccessible to us after a while.

- We aren’t getting anything that “can wait”. Some credit cards can wait; cards from Chase that I “can’t get later” should be a priority. If I can get a card later, I will focus on what I CAN’T get later.

But Which Card?

Now that we know we are going to apply for a card from Chase, the question becomes “which card?” They have a lot. We need to narrow it down. For most people in this hobby, the choice is between 1 of 2 cards. Here’s a breakdown on the comparison.

Chase Sapphire Preferred

The Chase Sapphire Preferred (often referred to as “CSP”) is one of the most popular cards in this hobby, and it’s for good reason. Here’s a look at its benefits, perks, fees, and the points we can earn.

- Annual Fee: $95

- Welcome Offer: earn 60,000 Chase Ultimate Rewards points after spending $4,000 in the first 3 months

- Earn 2x points per $1 on travel and dining

- Earn 1x point per $1 on everything else

- No foreign transaction fees

- Tons of insurance and protection perks

- Full review here

For a low fee, you get 60,000 points and a slew of travel protections. You also can earn double points on travel and restaurants, which helps your points add up quickly. You don’t get any fancy frills, but this is a good card.

Chase Sapphire Reserve

The Chase Sapphire Reserve (often referred to as “CSR”) is the 2nd of the 2 most common starter cards in this hobby. Here’s a look at its benefits, perks, fees, and the points we can earn.

- Annual Fee: $550

- Welcome Offer: earn 50,000 Chase Ultimate Rewards points after spending $4,000 in the first 3 months

- Earn 3x points per $1 on travel and dining

- Earn 1x point per $1 on everything else

- No foreign transaction fees

- Tons of insurance and protection perks

- $300 in annual travel credits

- Global Entry / TSA Pre-Check application fee reimbursement

- Priority Pass airport lounge membership

- Full review here

Don’t balk at the $550 fee. The first $300 you spend each year on travel will be credited back to your account. You get the $100 application fee for Global Entry or TSA Pre-Check credited back to you. And you get unlimited visits for you and 2 guests to airport lounges in the Priority Pass network. With free food and drinks there during your wait at the airport, you’ll save lots of money.

Making The Decision

The decision comes down to what you value. The Sapphire Preferred has less fringe benefits but comes with a lower fee because of that. It also has more points in the welcome offer. The Sapphire Reserve has more perks to justify its larger fee. Both are excellent cards and are favorites in this hobby for valid reasons.

If you have a partner, there’s another idea: get both. My wife applied for the CSR, and I got the CSP. We like to call this “two-player mode”. Both cards earn valuable Ultimate Rewards points, which you can do TONS of things with. See our guide here.

Decide which card is the best for you depending on what you value. If interested, I previously wrote a detailed explanation on how I decide which credit card to get next. It goes through some things that might be confusing when learning about points and miles for beginners, but it could be worth a read when evaluating future credit card applications.

Now that we know the cad we’re applying for, we are ready to apply.

Apply For The Card

You’ve chosen a card and are ready to apply. Fill out the application with all of your personal information. Then, check it again. Also, make sure you don’t have something like a fraud alert or credit freeze on your credit report. If so, you need to take action, or the bank won’t be able to process your application / view your credit report.

Ready? Is everything correct? WAIT. Before you hit ‘submit’, I recommend taking a picture. In case there’s ever any doubt about how much you need to spend, how many points you can earn, what date you applied, etc. you will have this. Take a screen shot. Now we’re ready. Submit the application.

If you are lucky, the application will be approved instantly. Congratulations! If it didn’t say you were approved, that doesn’t mean something is wrong. Applications can take a few days to work through the system. You can follow the steps in this article to check your credit card application status with Chase.

Did You Get Denied?

If you got denied, it’s not the end of the world. You will receive a letter in the mail explaining why you got denied. Could the bank not verify your address? Do they need proof of identity? They’re required to tell you specifically why you were denied.

Once you understand the reasons, you are ready for something called a reconsideration call. You’re asking them to reconsider your application after fixing the reasons for denial. Make sure you can specifically address those items, such as explaining past missed payments or change of address, etc. (whatever they mention in the letter). This isn’t impossible and should be straightforward as long as you were honest in your application.

Time To Start Keeping Notes

As I mentioned in the last article, you need to be organized. Now that you’ve applied for your first credit card, it’s time to write down the important information. Create a Word document, Excel sheet, or even use Travel Freely. Whatever it is, you want to know 1) how much you need to spend, 2) what points and miles you can earn from the welcome offer, and 3) the date you applied/deadline date for the spending. With most applications, the deadline is 3 months. I try to finish the spending at least a week before that, just to be sure all of the charges have cleared my account. Better to be safe than sorry!

Using Your New Credit Card

Once your new credit card arrives, follow the instructions to activate it. Set up your online banking. Now, start using the card!

But don’t be crazy. The goal is not to spend more money. The goal is to take everything you’re spending and put it on this new credit card. Think about what you spend every month. When you buy gas, eat at restaurants, pay your utilities…use this new credit card! In fact, there are even online services where you can pay your rent or mortgage with a credit card (for a fee).

Until you’ve passed the spending threshold (in our examples, $4,000 in 3 months), you should put every dollar possible on this new credit card. If anything gets returned, canceled or refunded, make sure you account for that. Going a little past $4,000 isn’t a bad idea, just in case.

Final Thoughts On Points And Miles For Beginners – Part 2

That’ll do it for Part 2 – Getting Your First Card. We built on our background research from Part 1 and then evaluated the 2 best starter cards for this hobby. We compared them, picked 1, and then we applied for it. We also talked about the possibility of getting one of them for yourself and the other for your spouse, which is a way to share the perks while keeping your fees down. You don’t both need the Priority Pass lounge membership, since one of you can bring the other as a guest!

We’ve applied for our card, and it should be coming in the mail soon. Once you’re approved and get the card, shift all of your current spending onto the card wherever possible. Make sure you keep things organized, so you know the requirements and deadlines for earning the points in the welcome offer. You’ve just started earning your first big bonus in the world of points and miles!

For next time:

Your homework for Part 3 of Points and Miles For Beginners is to have some type of organizational system. Use whatever works for you. Set it up to track the following:

- Date of application

- Date of approval

- Deadline date for welcome offer

- Points you can earn

- Spending amount required

- Annual fee and date it’s due

- Credit limit on the card

{kind=link}

Any suggestion for my 18 year old son. No cc’s. Likes going to movies with friends (i know can’t do that now) and enjoys eating out. He does a lot of takeout at this point. So was thinking Capital one Savor…

Then my 20 year old daughter who is in college. And wants to travel. Not sure which card for her. Ideas?

Brett – I’d still suggest the same thing for both of them. Starting with either CSR or CSP makes sense for a number of reasons. Take-out / restaurants will code as bonus points on either of those cards. Either one has points that can be used for flights, hotels, gift cards, cash back, etc. If your son has absolutely 0 desire to participate in this hobby, probably will never get another credit card ever again, etc. then I could see getting something like the Savor where he gets a good return rate on very specific items but then has limited options for anything else. If you want a card that does specifically 1 thing and does it well, it makes sense. If you want a card that has more than 1 perk, I wouldn’t go that route. For your daughter, I definitely would get the CSP or CSR for traveling.

These two sentences while intended to mean the same thing, actually describe different limits, one advises that if you’ve opened “more than 5” meaning 6 or more in 24, vs. the other advising less than 5 and you’re okay. Neither offers what happens when you’re at exactly 5 in 24. Suggest editing to clarify: “The 5/24 rule is from Chase … they will automatically deny you for any applications if you have opened more than 5 credit cards in 24 months. … versus …. As long as your number is under 5, we’re ok with Chase.”

Actually, the first does mean 5 or fewer is okay, while the second advisory sentence says you have to be under 5. Still needs some editing, respectfully.

Douglas – changed it to say “5 or more” to make it clearer. Thanks for the input.

Super, keep up the great work; I point newbees to your information all the time.

Awesome. Thanks!